Introduction:

Crypto tax in 2026 can feel messy, and you are not imagining it. Between IRS 1099-DA, digital asset tax filing, and the constant noise around new reporting rules, many U.S. investors are still unsure what counts, what does not, and what the IRS actually wants from them. If you are searching for cryptocurrency taxes in the USA, this guide keeps it simple, practical, and focused on what matters most: reporting correctly, avoiding mistakes, and keeping more of your money legally. The IRS is blunt here: you “must report all income, gains, and losses” from digital asset transactions.

Here’s the promise: this Crypto Tax 2026 guide will walk you through taxable events, tax-free activity, cost basis, forms, compliance, software, and legal ways to lower your bill without playing games. It is written for real people, not tax robots, so you can scan it fast, understand it fast, and actually use it when you file.

Why Crypto Tax 2026 Matters for U.S. Filers

The reason this topic matters so much now is simple: the IRS is paying closer attention, brokers are reporting more, and taxpayers still carry the final responsibility. IRS digital assets guidance says you must answer the digital asset question on your return, and Form 1099-DA is now the broker form used for digital asset proceeds from broker transactions. That means the old habit of guessing at your numbers is a bad idea.

IRS 1099-DA changes the reporting game

1099-DA explained in plain English, it is the form brokers use to report certain digital asset transactions to you and the IRS. The IRS says the form is used for digital asset proceeds from broker transactions, and current instructions say it applies to transactions beginning in calendar year 2025. That shifts the compliance burden upward, but it does not remove your duty to report correctly.

What U.S. investors must know first?

Before you think about strategy, you need the basic rule: the IRS wants digital asset activity reported, whether or not it results in a taxable gain or loss. The digital asset question must be answered, and the IRS expects accurate reporting for sales, exchanges, payments, rewards, and other dispositions. In other words, the paperwork matters, but the transaction history matters even more.

How Crypto Is Taxed in the U.S. in 2026

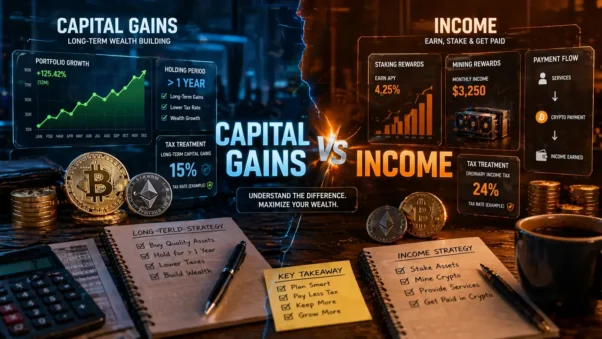

At the center of U.S. crypto tax rules is a simple split: some crypto activity creates crypto capital gains, and some creates crypto income tax. If you sell a capital asset for more than your basis, you may have a gain. If you receive crypto as payment, a mining reward, a staking reward, or similar income, that usually falls into ordinary income territory instead.

Capital gains tax vs ordinary income tax

This is where many people get tripped up. IRS property treatment means crypto is not treated like cash in most tax contexts, so the tax outcome depends on what you did with it. Sell it, swap it, or spend it, and you may create a capital gain or loss. Receive it for work, staking, mining, or rewards, and you may create ordinary income.

Short-term and long-term holding rules

The holding period matters because the tax bill can change a lot. The IRS says a gain is short-term if you held the asset one year or less, and long-term if you held it for more than one year. That is why short-term vs long-term crypto tax planning is not a fancy theory, airdrops, and DeFi income

This is where crypto income classification matters most. The IRS treats income from mining, staking, and similar reward activity as reportable income, and its digital asset guidance specifically points taxpayers to ordinary income reporting on the right return or schedule. If you earn crypto, you usually owe tax before you ever sell it.

What Counts as Tax-Free Crypto Activity?

Not every move is taxable, and that is a relief. One of the most important parts of IRS crypto reporting is understanding the difference between a real disposition and a simple transfer. If you move coins between your own wallets, that is usually not a taxable sale, though fees paid in digital assets can still create tax consequences.

Wallet-to-wallet transfers, you do not report

A transfer between wallets you own is not the same as selling. The IRS guidance on digital assets makes this distinction clear, and that matters because many people panic when they see a wallet move and assume they owe tax. You usually do not report the transfer itself, but you should still keep clean records.

Buying and holding without selling

If you buy crypto and simply hold it, you usually do not create a taxable event. That is the quiet part that many people miss. Buying is not the same thing as disposing, and holding is not the same thing as realizing gain. The tax story starts when you sell, swap, spend, or earn.

How to Report Crypto on Your U.S. Tax Return

Here is the practical part, the part that turns how to report crypto from a search query into an actual filing process. The IRS says capital asset sales and exchanges go on Form 8949 and then on Schedule D, while ordinary income from digital assets is reported on Schedule 1 or the relevant line of the return. That is the core map for digital asset reporting rules.

Form 8949 and Schedule D for gains

If you sold or swapped crypto that you held as a capital asset, you generally list those transactions on Form 8949 and summarize them on Schedule D. The IRS instructions also say to include these transactions even if you did not receive Form 1099-B, Form 1099-DA, or another statement. That is why your own records still matter.

Schedule 1 and other income reporting

If your crypto activity created ordinary income, you report it differently. The IRS says non-business ordinary income from digital assets goes on Form 1040, Schedule 1, or another applicable return line, depending on the filing situation. That includes rewards and similar income that does not belong on Schedule D.

How to Calculate Cost Basis Without Errors?

Your crypto cost basis is the part that decides how much gain or loss you actually have. In plain English, it is what you paid for the asset, adjusted for the transaction details that matter. If your basis is wrong, your gain is wrong, and that can mean overpaying tax or filing an inaccurate return.

FIFO, HIFO, and specific identification

This is where cost basis tracking gets serious. FIFO means first in, first out. HIFO means highest in, first out. Specific identification lets you choose a specific lot if you have the records to support it. The IRS says specific identification is allowed in some cases, and when it is not made, older units are generally treated as sold first.

Fees, transfers, and missing records

Fees can change your numbers more than people realize, especially when you move across exchanges and wallets. The IRS guidance says you need the fair market value, the basis, the date, and the transaction details to compute gain or loss properly. If records are missing, you need to rebuild the history carefully before filing.

How to Save Thousands Legally with Crypto Taxes?

This is the part readers actually want, the part where crypto tax compliance and savings meet. The goal is not to dodge tax; it is to avoid unnecessary tax. That means timing matters, lot selection matters, and loss planning matters. A small mistake can cost real money, while a clean approach can save a lot without creating drama.

Tax-loss harvesting and timing your sales

Let’s make this real. Say you bought ETH at $2,000 and sold it at $1,400. That creates a $600 loss. If you also sold BTC later with a $2,000 gain, the loss can help offset part of that gain. This is why crypto capital gains tax USA planning is often about when you sell, not just what you own.

Long-term holding and smarter lot selection

A patient move can work better than a noisy one. If you hold for more than one year, you may qualify for long-term treatment, which is usually friendlier than short-term treatment. Smarter lot selection can also reduce taxable gain when your records support it. In simple terms, don’t let the oldest, most expensive mistake become your default tax bill.

Crypto Tax Compliance Mistakes That Trigger IRS Issues

This is where crypto tax compliance becomes more than a phrase. The most common mistakes are not exotic. They are basic, boring, and expensive, missing income, bad basis numbers, transfer confusion, and mismatch problems with broker records. The IRS has made it very clear that digital asset activity still belongs on the return even when the paperwork is incomplete.

1099-DA mismatches and missing income

If your broker reports one number and your return shows another, you have a problem that deserves attention. The new reporting environment is designed to surface those mismatches faster. That is why IRS compliance for crypto now starts with reconciliation, not panic at filing time.

Audit red flags every filer should avoid

The biggest red flags are usually simple. Leaving the digital asset question blank, ignoring staking or mining income, treating transfers like sales, and using unsupported basis numbers are all avoidable. Strong records, clean reconciliation, and a sensible filing workflow reduce audit risk and make your return easier to defend.

Best Crypto Tax Software for 2026 Compliance

If you are handling more than a few trades, software can save time and reduce mistakes. The best crypto tax software 2026 options should help with exchange imports, wallet tracking, basis matching, and form exports. In plain English, a good tool should make your messy history readable again.

| Feature | Why it matters | What to look for |

| Exchange imports | Pulls trade history into one place | Strong support for major exchanges and wallets |

| Reconciliation | Matches transfers and catches gaps | Clear transfer detection and duplicate removal |

| Cost basis engine | Keeps tax math honest | FIFO, HIFO, and specific identification support |

| Form exports | Saves filing time | Form 8949, Schedule D, Schedule 1 output |

| Support | Helps with edge cases | Human review, CPA help, and error fixes |

A good crypto tax tracker or crypto tax calculator should also help you reconcile crypto transactions, import exchange transactions, and export U.S. tax forms without making you rebuild every trade by hand. That matters because good software is not just about speed; it is about cleaner records and fewer filing mistakes. If you use crypto compliance software or crypto filing software, look for a clean audit trail and easy transaction reconciliation.

FAQs:

Do I need to report every transfer?

No, not every transfer is taxable. A transfer between your own wallets is usually not a sale or disposition, but you should still keep records so you can prove what moved, when it moved, and what the original basis was. Fees paid in digital assets can still matter.

What if I did not receive Form 1099-DA?

You still may need to report everything. The IRS says taxpayers must report all income, gains, and losses from digital asset transactions, whether or not they receive Form 1099-DA. Missing the form does not erase the transaction history.

Is stakeholder income taxed in the U.S.?

Yes, staking rewards are generally reportable as income when received, based on IRS digital asset guidance. The important thing is to track the fair market value at receipt, then keep the record with your tax file. Later sale treatment is a separate step.

What is the safest way to track crypto taxes?

The safest approach is to keep every trade, wallet transfer, and reward in one organized record set. That means a clean tax audit trail, consistent basis tracking, and a simple method for matching exchange and wallet history before you file. Good records are boring, and boring is good here.

Can I file crypto taxes online?

Yes, and many people do. The key is to make sure your software or tax workflow can handle reporting cryptocurrency taxes in the USA, calculate crypto tax liability, and prepare the correct forms. Online filing is easier when your records are already reconciled, and your basis numbers are clean.

Ready to File Smarter with PrimePulseLogic?

If you want a cleaner path through Crypto Tax 2026, Prime Pulse Logic can help you turn a messy crypto history into something usable, understandable, and ready for filing. That means better reporting, fewer mistakes, and less money left on the table for no good reason. Visit https://primepulselogic.com/ review the guide again, and use the contact form to take the next step with your tax content or compliance workflow. Good crypto tax work starts with clear records, and clear records start now.